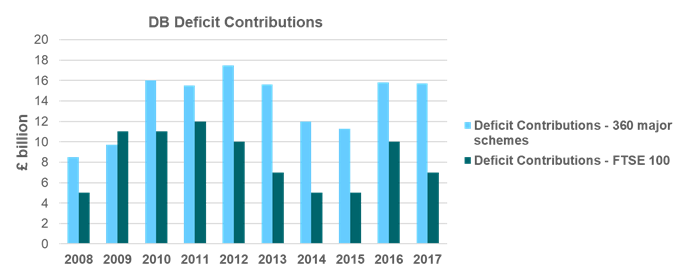

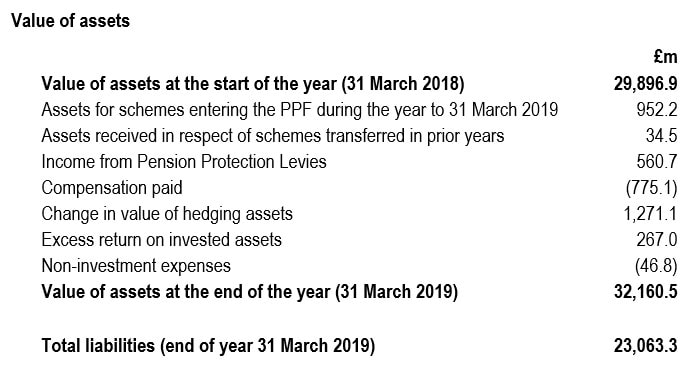

1. Defer agreed pension deficit contributions by 12 months, due in the year to April 2021. Consequently, all subsequent payment dates move forward by a year. This adds £13 billion to UK corporate liquidity in 2020 / 2021. If any sponsor subsequently does not make the payments then due in the year April 2021/2022 and enters an assessment period with the Pension Protection Fund, there will be a State Guarantee of that deferred amount payable to the scheme. This structure should ensure the Guarantee is not State Aid granted to the sponsor. Sponsors / trustees should consider third party, risk diversifying, payment guarantees from banks / insurers to back this deferral and/or longer term rearrangements of recovery plans. The deferral enables The Pensions Regulator to respond to its statutory obligation in respect of the sustainable growth of employers. DWP/TPR can take the initiative and state they will support company / sponsor agreements to make such deferrals. They would expect the parties to consider dividend payment levels to ensure fairness to all stakeholders. TPR should also ensure that the proposed 2021 Pension Funding Code takes account of changed economic circumstances created by Covid-19.  Approximately £140bn in DB pension scheme deficit contributions have been made by 360 major UK schemes in the 10 years to 2017  Contributions do not take account of the more stringent Long Term Funding Objectives required under the new Pension Funding Code 2. Pension Protection Fund suspends the levy for a year saving sponsors £550 million. The PPF is successful and strong financially with a substantial buffer within its £32bn asset base. The investment strategy and a much improved financial position of most defined benefit pension schemes means that its business model is profitable. It can reset its low dependency target date to 2035 rather than the current 2030. A year without levy contributions would not introduce material additional financial risk. An immediate policy focus should be on preventing schemes falling into the PPF because of Covid-19. A levy suspension helps. (Source PPF Funding Strategy Update 2018)  (Source PPF Annual Report and Accounts 2018/2019)  Related liabilities are £23bn. Schemes currently in assessment are considered to have a deficit of £3bn using a conservative basis on assets of £6bn.

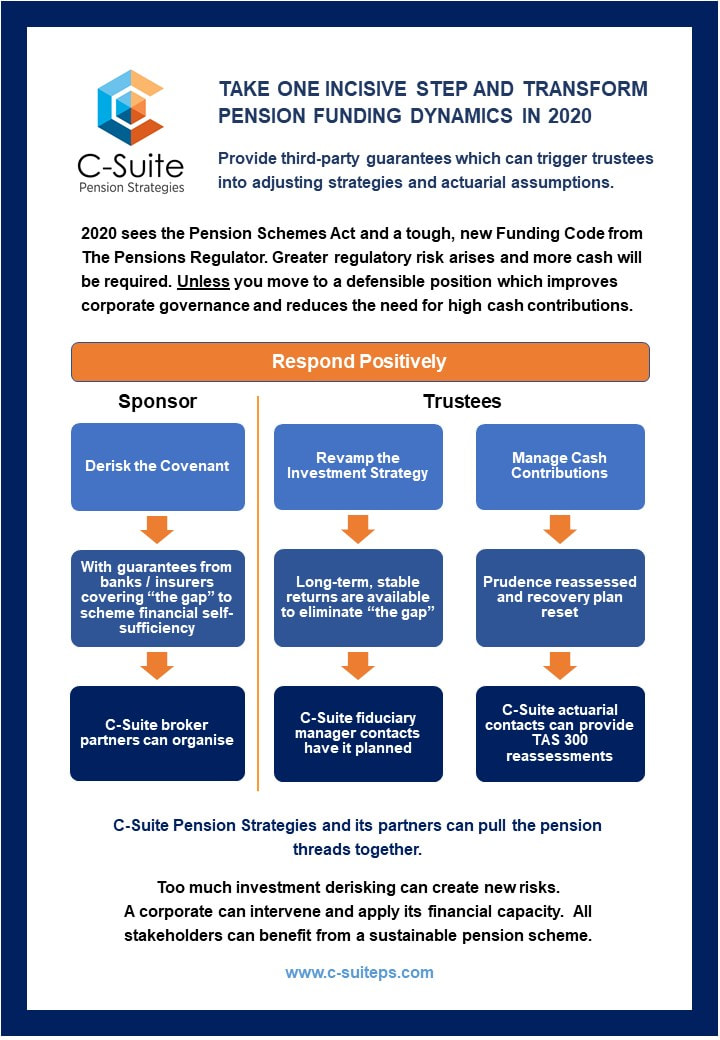

The Problem Statement Pension funding is bringing new reputational, governance, finance and accounting problems to Boardrooms. The Pension Schemes Act 2020 sets a tough regulatory framework. The mix of low interest rates and the derisking of investment returns is recognised as causing issues. Now, the funding targets set for schemes under The Pensions Regulator’s (TPR) new Funding Code are to move to self-sufficiency and buyout. Unless asset returns deliver the extra money, corporates will be paying considerably more in cash than their accounts currently suggest or actuarial deficits have been suggesting. Further, the “Stronger Pensions Regulator” can cut across corporates’ dividends, leverage and transaction plans. The powers are backed with reprimands, fines and criminal sanctions. But it also has a statutory obligation to support sustainable growth. It is now open to new initiatives and guarantees in bespoke solutions. The Solution Corporates can respond positively to the challenges posed and move decisively to a defensible position. Provide:

The Action Plan C-Suite Pension Strategies has the ideas and the actuarial and insurance sector contacts to make implementation possible The Government and TPR want action. Corporates can respond and all stakeholders’ benefit. Contact C-Suite Pension Strategies has an established network of senior executives from across the corporate and actuarial space – most particularly in banking and insurance. William McGrath, Founder of C-Suite Pension Strategies, ex CEO of Aga Rangemaster [email protected] |

Archives

July 2024

|

RSS Feed

RSS Feed

C-Suite Pension Strategies Ltd

80 Coleman Street, London EC2R 5BJ

Registered in England and Wales

Company No. 09974973

80 Coleman Street, London EC2R 5BJ

Registered in England and Wales

Company No. 09974973