The Discontents: Scheme members have some questions for trustees

|

|

Members’ Best Interests Involve Protecting Pensions' Real Value

Make 2023 Inflation Top Up Payment to the Pensions of Former and Current Employees

Trustees have worked hard to protect members form the remote risk of sponsor insolvency to their pensions. The high contributions; defensive investment; good governance are all part of it. Schemes also already pay for the highly effective PPF safety net. Yet still they aspire to the “peace of mind” offered by life insurers’ access to the unfunded Financial Services Compensation Scheme.

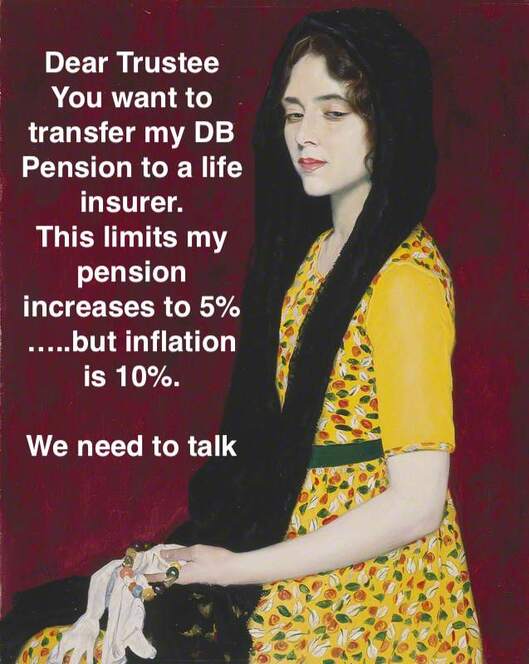

Trustees and sponsors should also address an immediate issue. This year’s DB pensions increase (the standard cap is 5%) is well below inflation (10% plus). There is for many a cost of living crises. The real value of the pension has fallen significantly. Can pension schemes help? Even if for one or two years only with standalone payments why not protect members from a real time problem?

Increases will need sponsor consent. Why should sponsors agree? Probably only if the increase has a finite cost to the scheme and is part of a rounded package. And it must not hit earnings.

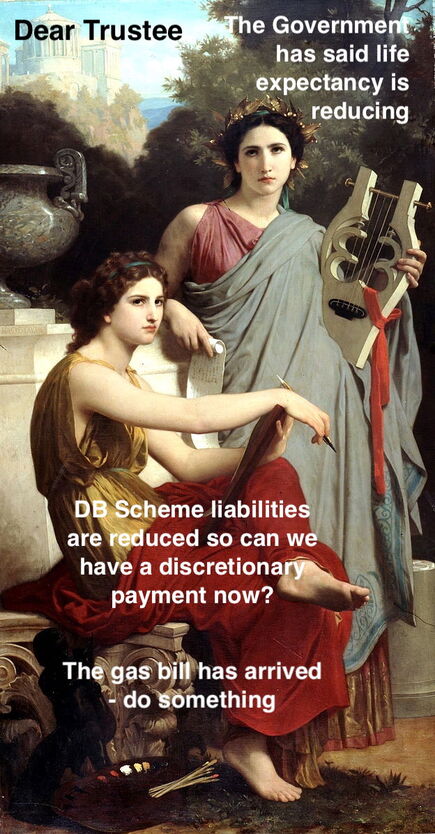

An Integrated Risk Management team of sponsor and scheme can see whether the administrative and cost barriers can be overcome in everybody’s interest. 2023 is unusual for the sharp change in interest rates and the coming downward revision in life expectancy of at least 6 months. It provides scope. Having a DB scheme can be a positive not a negative business feature reputationally and financially. The package can be:

The Integrated Risk Management team will look at the longer term framework for when and how surplus cash can be used by the trustees. This may involve the sponsor arranging third party guarantees to cover perceived downside solvency and investment risks. Then with a longer investment horizon the schemes are a worked example of Board and trustee ESG policies in practice. So being responsive to today’s employee issues fits well into a new Boardroom perspective.

Trustees have worked hard to protect members form the remote risk of sponsor insolvency to their pensions. The high contributions; defensive investment; good governance are all part of it. Schemes also already pay for the highly effective PPF safety net. Yet still they aspire to the “peace of mind” offered by life insurers’ access to the unfunded Financial Services Compensation Scheme.

Trustees and sponsors should also address an immediate issue. This year’s DB pensions increase (the standard cap is 5%) is well below inflation (10% plus). There is for many a cost of living crises. The real value of the pension has fallen significantly. Can pension schemes help? Even if for one or two years only with standalone payments why not protect members from a real time problem?

Increases will need sponsor consent. Why should sponsors agree? Probably only if the increase has a finite cost to the scheme and is part of a rounded package. And it must not hit earnings.

An Integrated Risk Management team of sponsor and scheme can see whether the administrative and cost barriers can be overcome in everybody’s interest. 2023 is unusual for the sharp change in interest rates and the coming downward revision in life expectancy of at least 6 months. It provides scope. Having a DB scheme can be a positive not a negative business feature reputationally and financially. The package can be:

- Add new power to trustees in the Scheme’s Rules to pay time limited increases unilaterally up to a new, higher inflation cap – when certain funded levels are in place.

- Pay inflation based discretionary increases for 2023 and 2024.

- Where the scheme is in actuarial surplus, pay an agreed amount to an existing / new DC tier within the scheme, being a proportion of company and employee contributions.

The Integrated Risk Management team will look at the longer term framework for when and how surplus cash can be used by the trustees. This may involve the sponsor arranging third party guarantees to cover perceived downside solvency and investment risks. Then with a longer investment horizon the schemes are a worked example of Board and trustee ESG policies in practice. So being responsive to today’s employee issues fits well into a new Boardroom perspective.

Members Can Put Inflation Related Discretionary Payments on the Pensions Agenda

DB pension peace of mind comes from inflation protection, not always from a sale to a life insurer

The DB pensions industry has a largely settled opinion that “derisk and get rid” is the right journey plan for most pension schemes. Members are told that here is “peace of mind” and that buyouts are the Gold Standard. This approach benefits actuarial consultants and life insurers.

Scheme members, current employees and scheme sponsors should all look harder at the alternative option of scheme revival on a modernised basis so it can operate in all stakeholders’ interests and over the long term.

Members should be asking more challenging questions of their trustees. Inflationary times may lead them to have a new view of their best interests and the security of their pension seen in real value terms. There is a cap on payments – usually at 5% and inflation is 10%. It is what the pension buys not the nominal amount that counts – as the Goode committee pointed out in 1992.

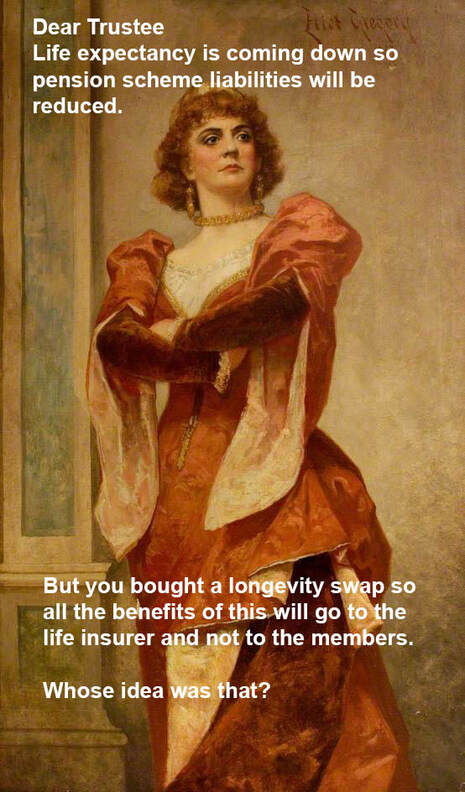

The risk assessment for members needs to be rerun. The downside is modest and measurable. There is the fully tested safety net of the well-run, well-funded PPF. It covers a large, increasing proportion of a pension. How the untested, unfunded Financial Services Compensation Scheme works is currently the subject of a Government review. With a buyout access to discretionary benefit improvements goes. The link to their former employer ends and the investment policies pursued are out of members’ control- just as ESG considerations come to the fore.

Solvency II replacement is much debated and creates uncertainty around concentration and systemic risk. There are also profound questions over future pricing as Government initiatives take hold. They are designed to improve pricing and increase competition. Wait and see is the sensible response.

Meanwhile corporate and member agendas have to move on. Most sponsors have committed to high standards of ESG. Pensions is a test case of those policies when in action. Does the large investment portfolio align with their green agenda? Do they see the scheme’s role in looking after the interests of former and current employees as important as their ESG statements indicate. Sponsors should be encouraged to stay the course and be leaders.

C-Suite Pension Strategies shows how available products can be combined to produce better outcomes. But what is really needed is for members and sponsors to question the negative pension sector mindset.

Transparency is needed. The losses arising from derisking are hidden away in sponsors’ accounts where they do not impact earnings. This means Schemes misreading of financial markets and longevity trends does not see the cold light of day. Certainly, the case for spending large sums on “derisking” from the members’ perspective should be restated more urgently cogently. And shareholders should wince at how their money has been spent. Consultants should be expected to provide data on actual transactions.

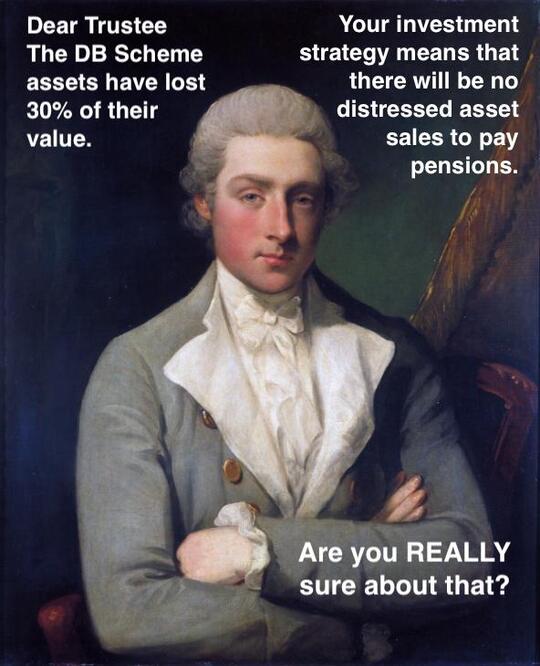

Current markets provide a good test case. Interest rate rises should have reduced actuarial liabilities – more scope for improvements? But not so fast. Matching asset will have fallen heavily in value. The scheme may be forced to sell return seeking assets to meet cash collateral calls under LDI programmes. Ironic if risk reducing measures stand in the way of discretionary payments to members.

“Decommissioning” is very often not in the best interests of members and does not provide “peace of mind”. When the Boards of sponsors embrace the schemes and do not abdicate responsibilities, a new and better settlement can emerge. When there is time made available all stakeholders benefit.

No discretionary increases while inflation reduces the value of pensions? Members should consider their position and revolt. Current employees should ask for surpluses to be used to boost current provision.

The DB pensions industry has a largely settled opinion that “derisk and get rid” is the right journey plan for most pension schemes. Members are told that here is “peace of mind” and that buyouts are the Gold Standard. This approach benefits actuarial consultants and life insurers.

Scheme members, current employees and scheme sponsors should all look harder at the alternative option of scheme revival on a modernised basis so it can operate in all stakeholders’ interests and over the long term.

Members should be asking more challenging questions of their trustees. Inflationary times may lead them to have a new view of their best interests and the security of their pension seen in real value terms. There is a cap on payments – usually at 5% and inflation is 10%. It is what the pension buys not the nominal amount that counts – as the Goode committee pointed out in 1992.

The risk assessment for members needs to be rerun. The downside is modest and measurable. There is the fully tested safety net of the well-run, well-funded PPF. It covers a large, increasing proportion of a pension. How the untested, unfunded Financial Services Compensation Scheme works is currently the subject of a Government review. With a buyout access to discretionary benefit improvements goes. The link to their former employer ends and the investment policies pursued are out of members’ control- just as ESG considerations come to the fore.

Solvency II replacement is much debated and creates uncertainty around concentration and systemic risk. There are also profound questions over future pricing as Government initiatives take hold. They are designed to improve pricing and increase competition. Wait and see is the sensible response.

Meanwhile corporate and member agendas have to move on. Most sponsors have committed to high standards of ESG. Pensions is a test case of those policies when in action. Does the large investment portfolio align with their green agenda? Do they see the scheme’s role in looking after the interests of former and current employees as important as their ESG statements indicate. Sponsors should be encouraged to stay the course and be leaders.

C-Suite Pension Strategies shows how available products can be combined to produce better outcomes. But what is really needed is for members and sponsors to question the negative pension sector mindset.

Transparency is needed. The losses arising from derisking are hidden away in sponsors’ accounts where they do not impact earnings. This means Schemes misreading of financial markets and longevity trends does not see the cold light of day. Certainly, the case for spending large sums on “derisking” from the members’ perspective should be restated more urgently cogently. And shareholders should wince at how their money has been spent. Consultants should be expected to provide data on actual transactions.

Current markets provide a good test case. Interest rate rises should have reduced actuarial liabilities – more scope for improvements? But not so fast. Matching asset will have fallen heavily in value. The scheme may be forced to sell return seeking assets to meet cash collateral calls under LDI programmes. Ironic if risk reducing measures stand in the way of discretionary payments to members.

“Decommissioning” is very often not in the best interests of members and does not provide “peace of mind”. When the Boards of sponsors embrace the schemes and do not abdicate responsibilities, a new and better settlement can emerge. When there is time made available all stakeholders benefit.

No discretionary increases while inflation reduces the value of pensions? Members should consider their position and revolt. Current employees should ask for surpluses to be used to boost current provision.

Contact

William McGrath, Chief Executive, C-Suite Pension Strategies

T: 07768 607204

E: [email protected]

TC Jefferson, Chief Executive The Plenum Group & C-Suite Partner

T: 07581 466620

E: [email protected]

William McGrath, Chief Executive, C-Suite Pension Strategies

T: 07768 607204

E: [email protected]

TC Jefferson, Chief Executive The Plenum Group & C-Suite Partner

T: 07581 466620

E: [email protected]